Download slides

Download slides

Truckload markets brace for stacked seasonal disruptions

Published: Thursday, May 07, 2026 | 09:00 AM CDT

On this page

The coming weeks mark the start of a dense sequence of seasonal and regulatory events that are expected to disrupt truckload markets and elevate execution risk as the second quarter of 2026 progresses. While these events occur every year, trucking capacity entering this period is materially tighter than in recent market cycles, increasing the likelihood that the impact of these events will compound.

Upcoming events impacting U.S. truckload shipping

While Mother’s Day freight is regionally concentrated, due to a sharp increase in demand to move flowers out of South Florida, it does create a ripple effect. The crush of outbound shipments creates competition for trucks, especially in the Southeast, tightening capacity and raising spot exposure ahead of the holiday.

In a looser market, these effects are typically short-lived. This year, however, trucking supply has less slack, increasing the risk of residual backlogs spilling into subsequent weeks.

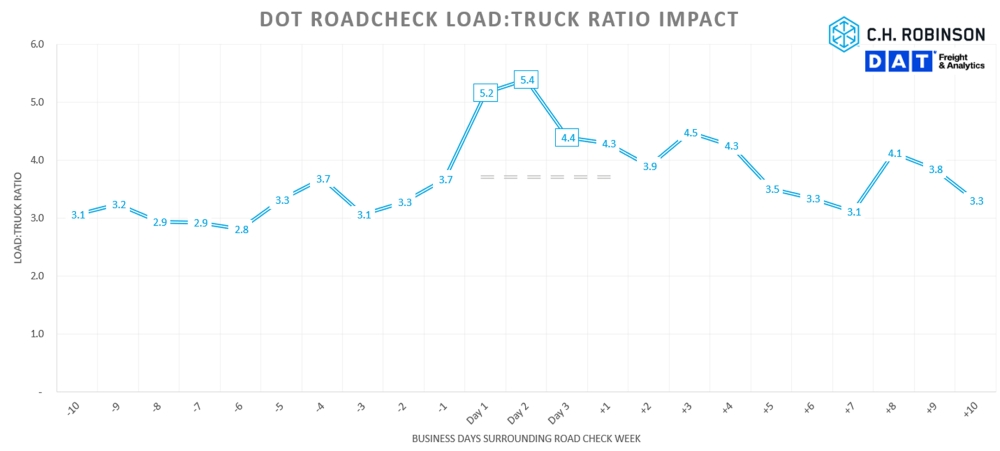

Immediately after Mother’s Day, the market transitions into Roadcheck Week May 12–14. Some carriers and drivers reduce their activity during this event to avoid the extended dwell time that comes with increased inspections. For 2026, Roadcheck Week inspections for drivers will emphasize electric logging device (ELD) tampering and hours of service falsification or manipulation. For vehicles, the focus will be on cargo securement.

Some drivers proactively take time off during the intensified inspection window, while others limit running in certain lanes. With regulatory enforcement already elevated this year, Roadcheck Week is expected to further constrain available capacity nationwide, particularly in border-adjacent markets.

DOT roadcheck load-to-truck ratio impact

Memorial Day adds another layer of friction. While it represents a single lost shipping day, the holiday often triggers a pull forward of freight and creates scheduling challenges around longer-haul moves that would otherwise transit the extended weekend. Combined with any unresolved backlog from Roadcheck Week, Memorial Day prolongs elevated spot-market activity.

Produce season in North America is the most well-known seasonal event that occurs each year as fruits and vegetables come to harvest in more areas. At the same time, beverages are in higher demand as consumers look to take advantage of the nicer weather. Produce volumes are ramping from Mexico and southern U.S. growing regions, including Texas, Arizona, California, and Florida, and will gradually move north as temperatures rise.

This year’s start has been slightly delayed by late freezes in the South, raising the risk that harvest activity becomes more compressed later in the season. As produce demand overlaps with regulatory and holiday disruptions, competition for trucks and drivers is expected to intensify across affected lanes.

Peak produce season by region

Individually, these events are disruptive and create a backlog of freight to work through once the event has passed. Together, they create a stacked disruption environment in which challenges are more likely to persist through May and into early summer.

Shippers should anticipate decreased tender acceptance, increased spot-market exposure, increased spot pricing, and tighter capacity as these seasonal factors unfold. Early planning, extended lead times, and proactive communication with your logistics provider will be critical to navigating these weeks effectively.

U.S. spot market

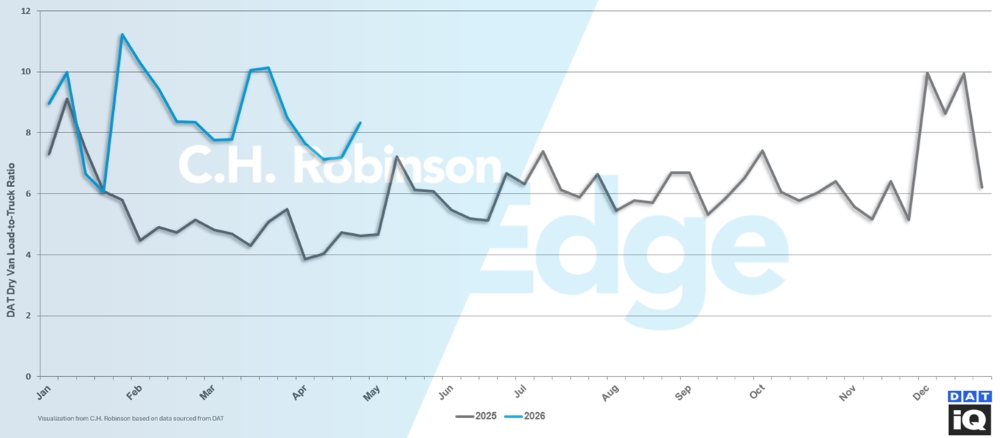

Carrier attrition continues, driven by elevated operating costs including fuel and a more restrictive regulatory environment. The DAT load-to-truck ratio increased the last week of April from 7.2-to-1 to 8.3-to-1, compared to last year when it decreased to a much softer 4.6-to-1.

As the market moves further into a period of supply‑driven tightening, upward pressure is being placed on spot rates. Rates typically ease as April progresses. This year, rates began to flatten in mid‑April and ultimately increased to close out the month. This shift indicates the seasonal upswing has started earlier than expected and highlights the stronger impact of tighter capacity on pricing.

DAT dry van load-to-truck ratio

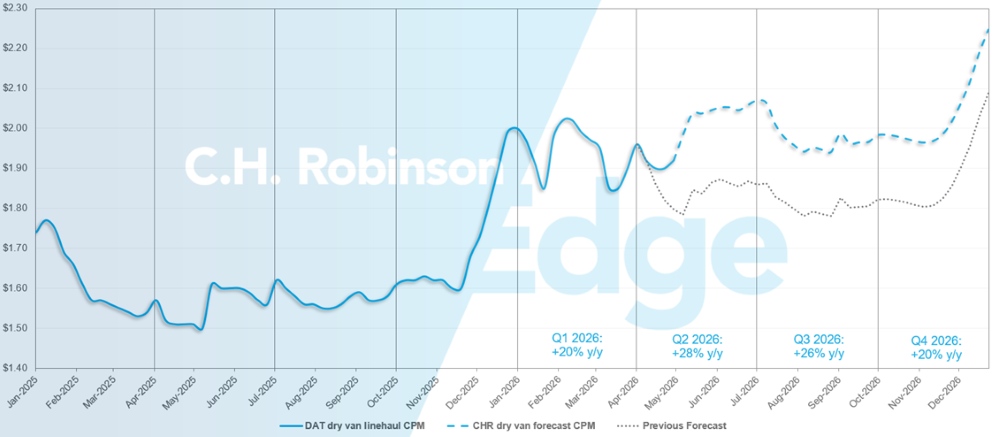

Based on these developments, and the divergence between expected and actual May starting conditions, the spot market forecast has been revised upward to better reflect current dynamics. While second‑quarter pricing is now expected to increase more than previously anticipated, the second half of the year is projected to follow a similar trajectory, albeit from a higher base.

U.S. spot market forecast: Dry van truckload

The C.H. Robinson 2026 dry van cost-per-mile forecast is being raised from +17% to +23% year over year (y/y).

C.H. Robinson spot market dry van truckload forecast

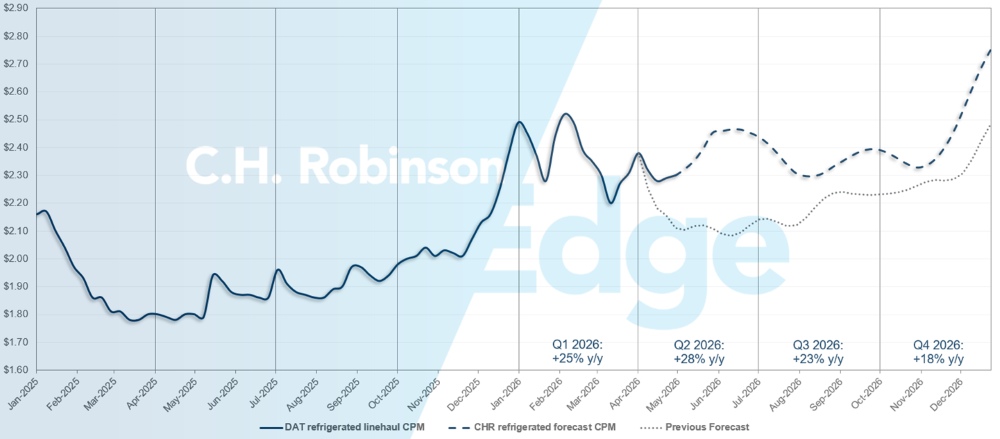

U.S. spot market forecast: Refrigerated truckload

The C.H. Robinson 2026 refrigerated van cost-per-mile forecast is being raised from +16% to +23% y/y.

C.H. Robinson spot market refrigerated truckload forecast

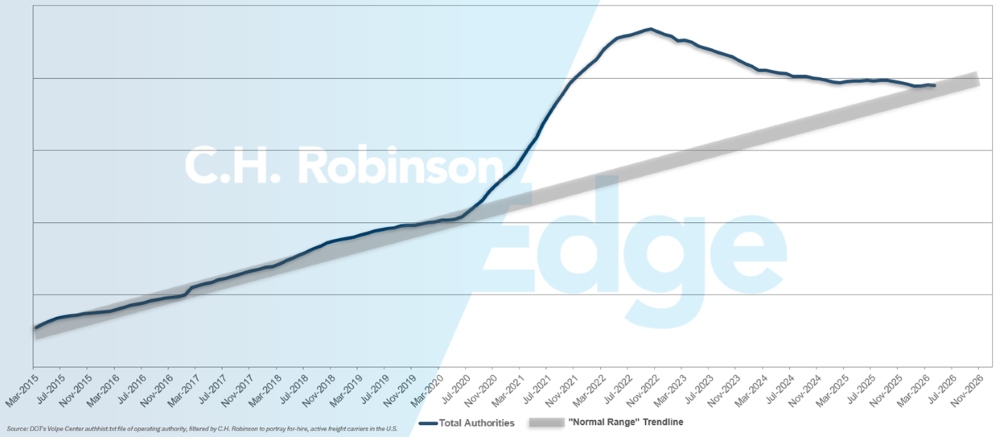

For-hire carrier authorities forecast

Carrier authority counts have returned to historical levels, reducing the excess slack that was previously available in capacity.

For-hire carrier forecast

Contract truckload environment

The following insights are derived from C.H. Robinson Managed Solutions™, which serves a large portfolio of customers across diverse industries.

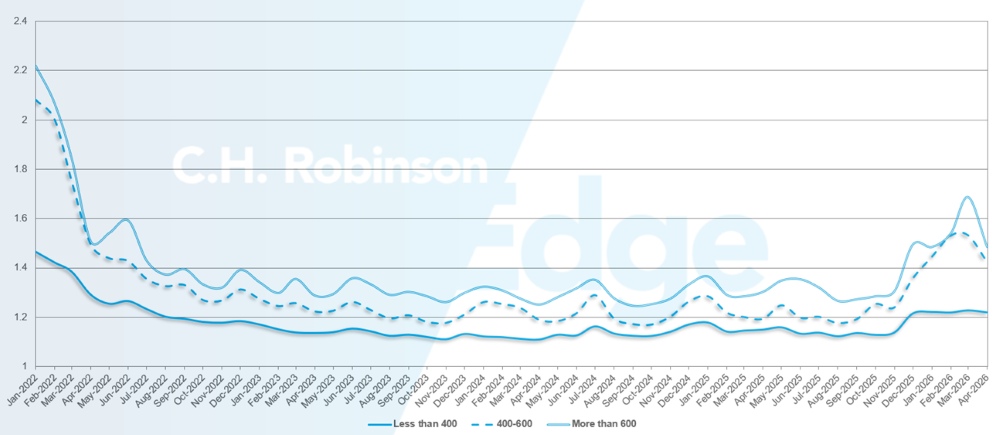

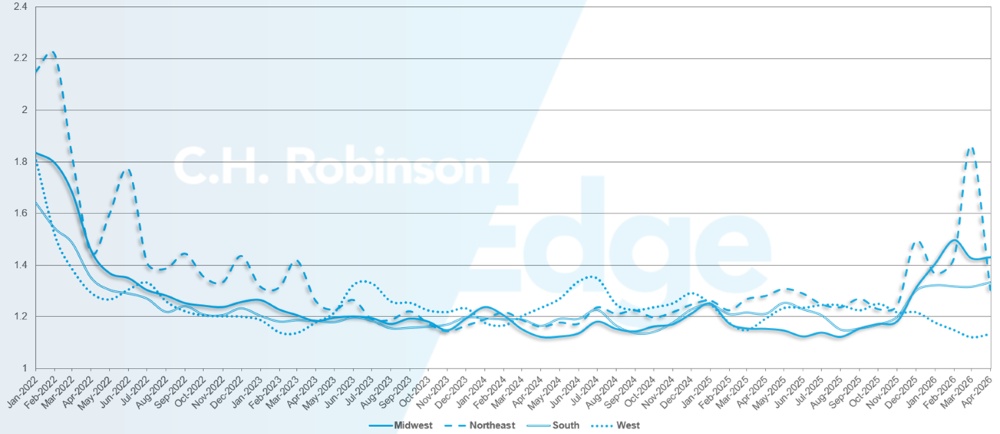

Route guide depth is an indicator of how far a shipper needs to go into their backup strategies when awarded transportation providers reject a tender. A route guide depth of 1.0 would be perfect performance, and 2.0 would be extremely poor. Route guide failures are when the route guide has been exhausted with no acceptance, sending the shipment into the spot market.

As displayed in the following chart, the route guide depth had remained flat at a historically low level for three years (2022-2025). Beginning in late November 2025, the first signs of a changing market showed up as route guide depth surpassed 1.3 for the first time in years. Since then, route guides have remained challenged due to a series of winter storms and increased diesel prices against a backdrop of decreasing capacity.

For the month of April, route guide depth across all North America shipments was 1.33, the lowest level of 2026.

From a mileage perspective, long hauls of more than 600 miles had a route guide depth of 1.49 in April, which is improved from the prior month of March 2026 at 1.69, but worse compared to April 2025, which was at 1.30. For shorter hauls of less than 400 miles, the route guide depth for April 2026 was 1.122, which is slightly better than the previous month of 1.123 but slightly worse than April 2025 at 1.15.

North America route guide depth metrics: By length of haul

Geographically, the Midwest experienced the smallest change of all regions, remaining flat from the previous month, while the Northeast experienced the largest change at 3%. Route guide depth varies significantly by region, between 1.13 and 1.43.

U.S. route guide depth metrics: By region

Refrigerated truckload

East Coast United States

Refrigerated markets along the East Coast are entering a period of heightened volatility as seasonal demand stacks on top of existing capacity constraints. Mother’s Day is driving concentrated demand in South Florida, particularly for floral shipments, tightening refrigerated availability across outbound lanes.

This pressure is unlikely to clear cleanly before the market moves into DOT Roadcheck Week May 12-14, when intensified inspections are expected to sideline drivers and reduce effective capacity nationwide. Heightened regulatory enforcement may further tighten capacity during this time.

While outbound Southeast loads are expected to be extremely challenging this May, it does provide an opportunity for decreased inbound costs for shippers as carriers look for backhaul. Taking advantage of this highly desirable corridor will mean low-priced options and ample capacity. This opportunity will begin to wane in June and dissipate in July, so swift planning is encouraged.

Central United States

As harvest season begins to peak for Mexico cross-border shipments as well as South Texas markets, refrigerated equipment will become increasingly scarce. This dynamic is expected to become more pronounced as the month progresses and overlaps with Roadcheck‑related supply disruptions.

While Central U.S. refrigerated demand itself remains more stable, shippers should expect increased competition for capacity and less tolerance for load inflexibility. As produce volumes advance into the Midwest later in the season, volatility is likely to persist, particularly on lanes connecting Central markets to coastal population centers.

West Coast United States

West Coast refrigerated markets are transitioning directly from spring agricultural activity into a heavier seasonal load environment. California and Arizona are seeing increasing refrigerated demand tied to produce season, specifically with the following commodities from each region:

- Nogales, Arizona: melons

- Lodi/Stockton, California: cherries

- Central Valley: citrus and stone fruit

- Salinas Valley: leafy greens and strawberries

- Santa Maria & Coachella: broccoli and peppers

As those volumes build, competition for refrigerated equipment is intensifying, particularly on longer‑haul outbound lanes. Combined with elevated fuel costs and lingering border‑related constraints, these dynamics are expected to keep West Coast refrigerated capacity tight through May and into early summer, although there is potential from some short-term relief out of the Pacific Northwest before cherry harvest begins there in late May.

Shippers should anticipate volatility in both tender acceptance and spot rates as produce flows overlap with regulatory and holiday disruptions. Longer lead times and flexibility will be key to success.

Flatbed truckload

Flatbed market conditions continue to reflect a seasonally tight environment as prime construction season progresses. Capacity constraints and regional imbalances are driving sustained competition for trucks, particularly across core construction and industrial corridors.

Roadcheck Week is expected to disrupt market conditions in May. This year’s emphasis on cargo securement is especially relevant for flatbed operations. As a result, temporary capacity tightening, increased rate volatility, and potential transit delays are expected during and immediately following the inspection window.

Holistically, flatbed market conditions remain elevated across key regions at this time of year. National load‑to‑truck ratios have held relatively steady week over week near 72 to 1, though pronounced regional disparities persist. The South and Southwest remain the most constrained, with the Texas‑to‑North Carolina corridor averaging load‑to‑truck ratios near 116 to 1.

While conditions remain tight and are expected to stay so through mid to late July, there are early indications the market may be moving off peak levels of stress. Carrier behavior continues to reflect caution, as multiple years of unfavorable market conditions have limited investment and delayed meaningful capacity expansion.

Demand signals across core flatbed sectors remain mixed. Builder confidence for newly constructed single‑family homes declined four points to 34 in April, reflecting continued caution in the residential construction market. At the same time, manufacturing activity has shown modest improvement.

According to the Institute for Supply Management, U.S. manufacturing leveled off in April at the same reading from March: 52.7. On this index, a number over 50 indicates expansion. Manufacturing expansion is helping support industrial freight demand and offset softer residential construction activity. As detailed in the Energy industry insights in this report, data centers and battery manufacturing are also impacting flatbed and heavy-haul demand.

Looking ahead, flatbed capacity is expected to remain volatile through July, with short‑term swings driven by seasonal demand and weather patterns. Broader indicators suggest the market may be moving past peak pressure, as building-product inventories appear largely replenished based on recent spot-market activity and historical trends.

While elevated load-to-truck ratios are expected to persist through the summer, that tightness is likely to gradually moderate mid‑summer.

What to do

In this environment, planning and flexibility remain critical to maintaining service and managing costs.

- Increasing lead times, where possible, can improve coverage, particularly during Roadcheck Week and peak seasonal periods.

- Allowing flexibility in pickup windows and ship dates can expand carrier options and reduce exposure to short‑term rate volatility.

- Broadening equipment flexibility, where feasible, can support coverage. Utilizing step decks or Conestoga trailers in addition to standard flatbeds may increase available capacity.

- Maintaining close coordination with your C.H. Robinson account manager can help you monitor regional shifts and position freight more effectively through a period of continued market volatility.

Voice of the Carrier

Observations from a cross-section of the contract carriers in the C.H. Robinson network—the largest in North America.

Market

- Capacity is tightening, driven by carriers leaving the market and labor constraints.

- Contract pricing is increasing and freight priced below market is being rejected in favor of more market-aligned freight.

Drivers

- Recruitment for long-haul drivers is becoming increasingly difficult.

- Recruitment and retention tactics such as driver referral programs, signing bonuses, targeted wage increases, and providing more time at home have become necessary.

Equipment

- Equipment availability is not a major constraint; trucks and trailers are generally available.

- Some carriers have begun to resume standard replacement cycles.

Actionable freight insights

Actionable freight insights