Download slides

Download slides

Port and inland execution conditions remain uneven

Published: Thursday, May 07, 2026 | 09:00 am CDT

On this page

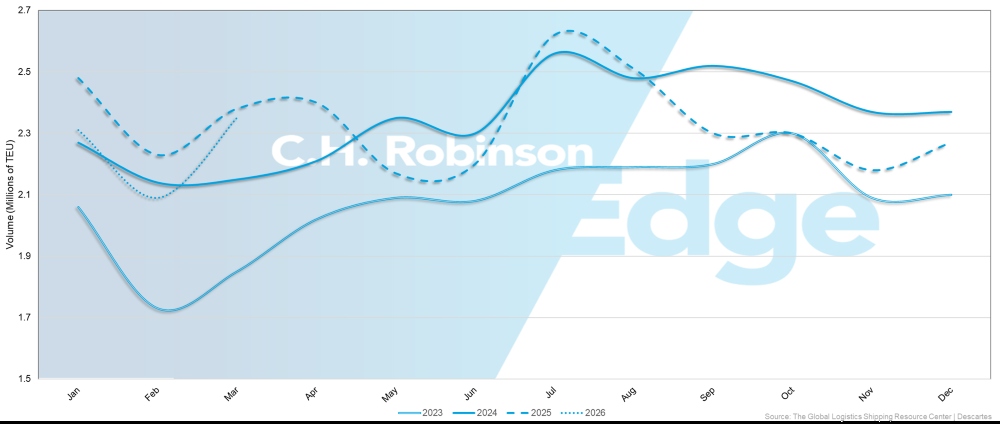

Clustered vessel arrivals are creating uneven gateway pressure

The pattern of arrivals—not sustained congestion—is the primary factor shaping port and inland network conditions this month.

Recent U.S. import volume trends support this view. Volumes remain within normal seasonal ranges. It’s service routing changes and blank sailings across major east‒west lanes that are contributing to bunched vessel arrivals into many North American gateways.

Unlike sustained congestion, clustered vessel arrivals create uneven demand for chassis, tighter appointment windows, and reduced turn-time consistency at intermodal facilities—even where overall throughput remains stable.

During peak arrival windows at major coastal gateways including Houston, Los Angeles/Long Beach, New York/New Jersey, and Savannah, clustered vessel arrivals are tightening chassis availability and appointment access. These short-cycle pressure periods are expected to continue shaping drayage planning at several gateways.

Inland impacts are becoming more visible as well, particularly across intermodal facilities where uneven arrival waves are reducing turn-time consistency and affecting driver productivity across ramp networks. These effects may continue influencing inland routing and scheduling decisions during May as arrival timing variability moves through connected rail flows.

U.S. import volume trends

Drayage costs remain elevated despite mixed demand signals

The National Drayage Spot Market Index is currently tracking roughly 8% higher year-over-year (y/y), with increases tied primarily to routing disruption, clustered vessel arrivals, tighter appointment windows, and higher operating costs rather than a typical spring demand surge.

Execution conditions continue to vary by terminal and inland ramp location, meaning network-level capacity trends do not always reflect local service reliability.

Chicago remains the inland ramp watchpoint

Out-gate congestion in Chicago continues affecting ramp fluidity despite recent infrastructure investments and appointment-system adjustments.

Norfolk Southern Landers continues reporting elevated out-gate delays, with roughly one quarter of loads exceeding two-hour thresholds. Performance remains mixed across the broader metro ramp network, with CN Harvey showing improvement y/y and CSX Bedford Park maintaining comparatively stronger throughput conditions.

These differences reinforce the importance of ramp selection when planning inland intermodal routes through the Chicago gateway complex.

Canadian inland timing remains seasonally variable

Across Canada, railcar availability constraints linked to winter deployment programs continue influencing Canadian inland point intermodal (IPI) timing. These effects remain consistent with normal spring operating patterns and are being offset by stable demand levels across the network.

Terminal performance at Halifax continues to improve after earlier weather-related disruption, helping prevent broader congestion from developing. At the same time, Ontario and Québec spring thaw trucking restrictions remain in effect and may introduce localized transit-time variability, particularly for heavier shipments.

Overall impacts remain limited, with minor timing adjustments rather than sustained execution disruption.

Diesel volatility creates brief relief windows, not sustained cost stability

Diesel prices have remained volatile in recent weeks as a nearly three-week decreasing trend was effectively wiped out with a sharp price increase the week of May 4, underscoring fuel’s continued role as a key cost pressure in drayage operations. Periodic pullbacks in diesel pricing, like experienced in late April, can provide short-term relief, particularly as fuel surcharges adjust downward and offer brief windows of improved cost alignment. However, those benefits have proven to be uneven and short-lived amid a broader environment of elevated and unpredictable fuel costs.

As a result, while periods of fuel cost relief are directionally positive for drayage economics when they appear, they do not fundamentally alter the underlying cost structure. Structural cost drivers—including chassis availability, labor conditions, terminal productivity, and appointment access—remain the primary influences shaping drayage execution outcomes across gateway networks.

Planning ahead

- Expect terminal fluidity to continue varying w/w at major U.S. gateways. Staggered vessel arrivals translate into uneven drayage demand rather than sustained congestion conditions.

- Allow additional flexibility around Chicago intermodal moves. Out-gate delays at selected ramps continue influencing driver productivity and turn-time consistency.

- Monitor single-chassis move assumptions on lanes where chassis splits are increasing. Rising chassis split frequency across parts of the Chicago ramp network signals increasing interruption risk.

- Plan for minor timing variability across Canadian IPI lanes. These conditions are expected to continue throughout the spring transition, especially affecting inland flows linked to Ontario and Québec.

- Expect fuel surcharge predictability to improve following recent diesel benchmark declines. Broader drayage pricing conditions will continue reflecting appointment access, labor availability, and terminal productivity factors.

Notable shifts this month

Chassis split frequency signals rising drayage friction

Rising chassis split frequency across parts of the Chicago ramp network is signaling increasing disruption to routine drayage moves. When containers cannot remain on the same chassis through pickup, delivery, and return cycles, additional gate transactions and driver time can increase total move cost even where headline capacity indicators appear unchanged.

This signal suggests recent yard-flow and appointment-system adjustments are not yet translating into consistent efficiency gains across all facilities.

Hamburg and Rotterdam remain bottleneck watchpoints

Elevated yard density and recent weather-related disruption earlier in the spring continue influencing arrival sequencing through Hamburg and Rotterdam. This is contributing to schedule variability across Asia–Europe and Trans-Atlantic services.

Southern Brazil congestion remains localized

Port operations across South America’s East Coast remain broadly stable, but localized congestion driven by elevated yard utilization and operational constraints continues affecting Itapoá and Paranaguá. Berthing delays of roughly four to seven days remain a planning consideration for cargo moving through southern Brazil gateways.

Callao-Chancay inland coordination remains Peru’s primary execution constraint

Peru maintains strong maritime connectivity across multiple gateway options including Callao, Paita, and Pisco. However, inland coordination across the Callao–Chancay corridor continues to represent the primary constraint affecting end-to-end shipment timing.

Although not caused by port congestion conditions, these landside bottlenecks remain an important planning consideration for cargo moving through Peru’s primary logistics corridor.

Key takeaways

- Monitor Chicago ramp selection carefully on inland intermodal moves. Variations in provider performance are impacting the consistency of turn times throughout the metropolitan network.

- Track chassis continuity assumptions on inland drayage moves. Rising split frequency signals increasing interruption risk within otherwise routine pickup–delivery cycles and may affect driver productivity and total move cost.

- Allow additional planning flexibility for cargo routing through southern Brazil. Berthing delays at Itapoá and Paranaguá continue to influence schedule reliability across portions of the South America East Coast (SAEC) network.

- Monitor landside coordination exposure on Peru gateway moves. Inland bottlenecks along the Callao–Chancay corridor remain the primary execution constraint despite strong maritime connectivity at Callao.

Actionable freight insights

Actionable freight insights