Download slides

Download slides

Diesel supply volatility adds supply chain risk

Published: Thursday, May 07, 2026 | 08:30 AM CDT

As the second quarter unfolds, energy markets are adjusting to a prolonged disruption in the Middle East rather than a short‑lived shock. A working assumption is that the Strait of Hormuz will remain effectively closed, tightening energy supplies and extending disruption well beyond immediate headlines.

Even if oil and diesel flows resume, delivering lanes for refineries would require weeks to normalise, marine insurance costs remain elevated and import dependencies reassert themselves. Diesel remains the dominant input for over‑the‑road freight globally and volatility in its availability is emerging as the strategic risk to watch.

Regional diesel fuel trends

In North America, U.S. diesel inventories sit below seasonal norms but have not crossed crisis thresholds. Prices, however, have moved sharply higher and carriers feel friction when fuel surcharge increases lag rapid diesel price increases. While fuel is typically treated as a pass‑through, timing gaps, imbalanced lanes and higher deadhead miles compress carrier margins.

Export demand is beginning to matter more as well. As overseas markets tighten, U.S. and Canadian barrels become increasingly attractive, subtly pulling supply outward. Exports of U.S. distillates recently hit a multi-year high with increasing deliveries to Europe. Availability holds for now, but global demand dynamics increasingly influence North American balances.

Mexico sits at the other end of the spectrum. Heavy import dependence and limited refining flexibility mean that diesel availability is tightening earlier. Canada broadly mirrors the situation in the United States, though eastern Canada is more exposed given higher import reliance.

Europe’s diesel market is less forgiving. Refineries are running overtime to meet baseline diesel and jet fuel needs. While alternative fuels are more common than in North America, Europe’s freight fleet remains overwhelmingly diesel‑powered and with limited inventory buffers, the region feels disruption almost immediately when crude flows tighten.

Jet fuel markets are already showing signs of critical strain, while higher marine fuel costs and longer ship routes ripple through logistics networks. The trend here is material tightening, with elevated volatility becoming the defining feature of the quarter rather than a transient spike.

Liquified natural gas and compressed natural gas provide limited cushioning in parts of Asia and China, but long‑haul freight globally remains diesel dependant. Asia has already moved toward conservation measures. China stands apart as government control over refining runs, export quotas and inventory allocation has kept domestic fuel availability relatively stable, allowing China to absorb the disruption.

Broader fuel considerations

Under the assumption the Strait of Hormuz remains closed, the broader outlook is fragmentation rather than normalisation. Inventories will draw down unevenly across regions as governments and refiners prioritise domestic supply and limit exports.

Countries with strong policy control and more diversified fuel portfolios (e.g., China) can absorb some of the shock. Import‑dependant, diesel‑dominant regions (e.g., Australia) face a more operational challenge, where allocation and prioritisation determine what moves and at what cost.

Electrification, while advancing, remains immaterial outside of urban, port and short‑haul use cases. Smart Freight Centre insights point to an important directional signal: electrified powertrains and hydrogen pilots are emerging as complements to diesel engines, not yet substitutes.

Infrastructure build‑out, manufacturing commitments and regulatory pressure suggest electrification will shape future resilience. But today’s freight networks still run on petroleum distillates.

What this means for shippers

Fuel volatility is no longer just an operating cost variable; it is a strategic risk input that shapes capacity, pricing and service reliability across regions and transportation modes. Stress‑testing assumptions, understanding regional tightening sequences and monitoring allocation signals matter as much as headline price movements.

Efficiency, fuel diversification and emerging low‑carbon solutions may not solve today’s disruption, but they increasingly define how resilient tomorrow’s supply chains will be.

North America fuel trends

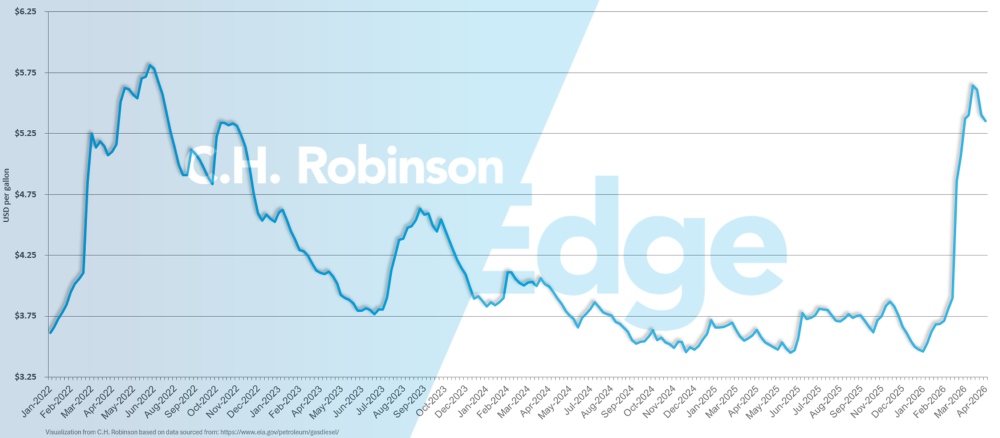

The national U.S. average diesel price per gallon of $5.50 in April was up from $4.92 in March. In addition to the increase in price month-over-month, the average price is also much higher than the April 2025 price per gallon of $3.57. Fuel has historically never been this high, except for May and June of 2022.

U.S. average diesel price per gallon

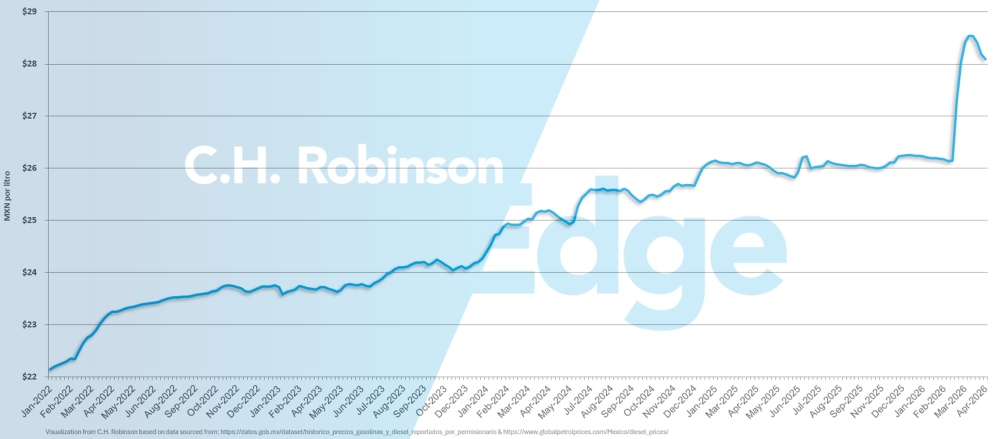

The national average diesel price in Mexico, shown here in Mexican pesos per litre, has spiked to approximately 28 pesos in recent weeks.

Mexico average diesel price per gallon

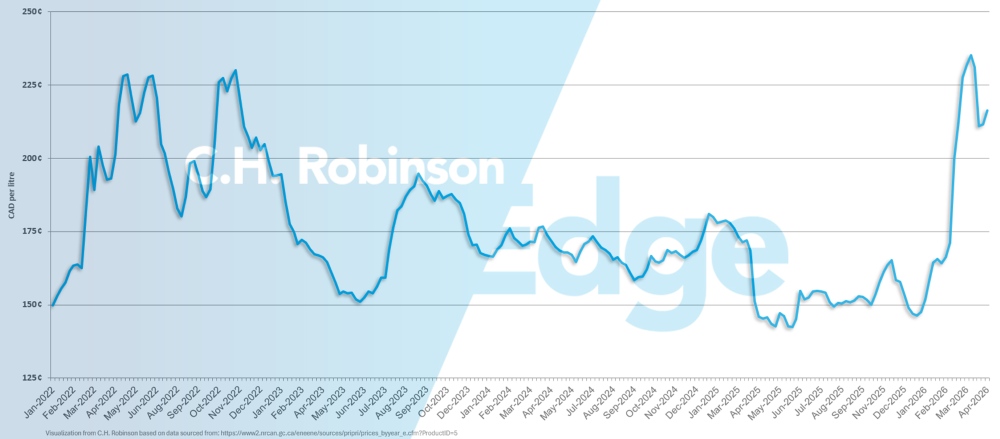

The national average diesel price in Canada, shown here in Canadian cents per litre, has decreased in recent weeks, but remains high historically.

Canada average diesel price per gallon

Actionable freight insights

Actionable freight insights