Download slides

Download slides

Early peak season impacts ocean freight planning

Published: Wednesday, July 01, 2026 | 09:00 am CDT

On this page

Ocean capacity tightens around an early, uneven peak season

July ocean freight is not moving in one synchronized peak-season market. Some lanes are seeing cargo pulled forward by seasonal demand and anticipation of higher U.S. tariffs. Others are constrained by service string withdrawals, blank sailings, port omissions, or container shortages. In several trade lanes, the important question is not how tight capacity becomes, but how long that pressure lasts.

For shippers, July planning should focus on the source of the constraint, because that determines how early shippers should book and how much routing flexibility is needed to keep their freight moving. A lane where capacity is tight because of sustained demand requires a different booking strategy than one affected by cargo pull-forward or temporary disruption. The strongest advantage will come from knowing which pressure is likely to hold, which may fade, and where conditions could shift quickly.

Conditions may ease where port congestion improves, blank sailings decline, or European summer slowdowns reduce shipment activity. Pressure may persist where capacity controls remain in place, equipment stays short, or service changes keep available space below what schedules appear to show.

Pull-forward demand is changing the shape of peak season

U.S. import volumes rebounded in May, with containerized imports reaching 2,428,758 20-foot equivalent units (TEUs), up 6.6% from April and 11.5% year over year. That recovery aligns with normal seasonal growth, but July demand is being shaped by more than seasonality.

Retailers are bringing cargo forward to manage rising shipping costs, fuel pass-throughs, and tariffs. The result is an earlier and more uneven peak-season setup, where volume recovery, cargo pull-forward and limited booking flexibility are converging before traditional peak season.

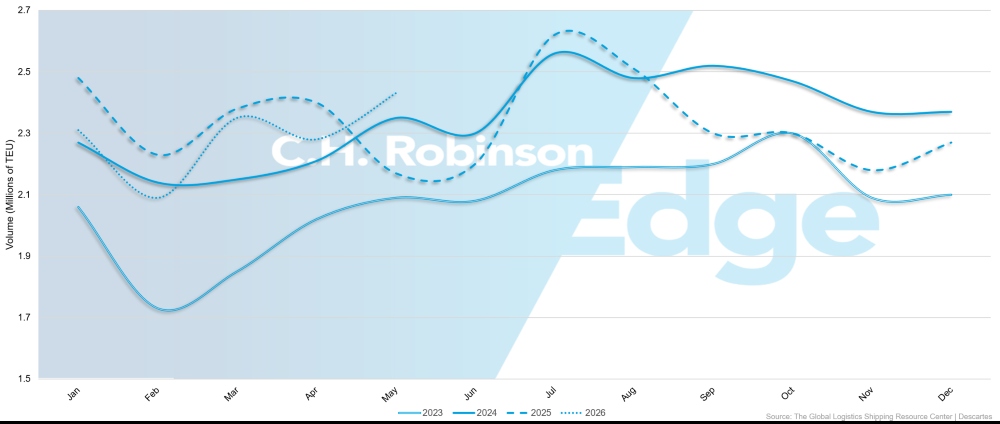

U.S. container import volumes, 2023–2026

The graphic illustrates the timing issue for July planning. As U.S. import momentum recovers, ocean capacity will be influenced by how much demand has been pulled forward, how long it remains in the market, and which lanes are most exposed when early cargo moves into already limited booking windows.

On the Trans-Pacific, spot rates continue to rise and are expected to remain elevated through July as peak-season cargo moves. China–U.S. exports of artificial intelligence (AI)-related technology and renewable energy equipment are adding volume into a market that already has limited room for late bookings. Conditions are especially tight on U.S. East Coast (USEC) and Gulf routes compared with the U.S. West Coast (USWC).

Asia–Europe is showing a different version of the same timing issue. Rates have continued their upward momentum from June, and carriers are pursuing another round of July increases. Space is expected to remain tight through mid-July across both north Europe and Mediterranean routes.

However, congestion in China and Europe has started to improve, and blank sailings are expected to decline in the coming weeks. Given the Asia–Europe demand surge began earlier than usual, especially into the Mediterranean, the peak may also moderate earlier than a standard seasonal cycle.

That makes July buying decisions more timing-sensitive. Higher spot rates may hold in some lanes, but not necessarily across the full market or for the same length of time. Shippers should watch whether demand continues, blank sailings ease, and operational conditions normalize before assuming current July pricing and space will carry forward.

Service withdrawals earlier in the year are being felt now

Pressure on available space is also coming from the way vessel capacity has been removed, redirected, or restricted, not from demand alone.

The Trans-Atlantic westbound lane is the clearest example. Rates are holding at higher levels and space remains tight, but the change is not being driven by a broad surge in cargo. It follows capacity reductions that began earlier in the year, after rates reached very low levels in late 2025 and early 2026.

Blank sailings remain part of the market, with approximately 9% of Trans-Atlantic westbound capacity blanked over the coming weeks. Bookings from north Europe are running three to five weeks out to the USEC and four to six weeks out to the USWC.

That gives Trans-Atlantic westbound a different planning profile than Trans-Pacific eastbound or Asia–Europe. On those trade lanes, stronger seasonal volumes are contributing to higher spot rates and tighter booking conditions. On Trans-Atlantic westbound, capacity removal is doing more of the work. Getting space may begin to ease in the second half of July as European summer vacations reduce shipment activity, but extended booking windows may persist if blank sailings and service adjustments remain in place.

The Indian Subcontinent shows how service changes can tighten a market as demand recovers. Mediterranean Shipping Company (MSC) has suspended its Indus Express service to the USEC, while CMA CGM has withdrawn the CJX service from south India and is relying on INDAMEX to serve USEC cargo. MSC has also withdrawn its Carioca service, shifting south India–South America East Coast cargo through alternate routings.

These changes are narrowing available space across India–U.S. lanes, particularly as seasonal demand recovers. Several carriers have implemented space allocation controls and booking restrictions on selected sailings, especially from northwest India. Peak season surcharge and general rate increases have followed, and shippers should secure India–U.S. bookings at least four weeks in advance.

A similar pattern is emerging on India–Europe. Space remains tight, spot and freight all kinds (FAK) rates have risen sharply, container shortages are expected to persist at major Indian export gateways, and shippers should book at least three weeks in advance. The constraint is not vessel space alone. It is the combination of service withdrawals, equipment imbalance, and carrier controls converging just as peak-season demand begins.

Oceania tightens as schedule disruption reduces available space

Oceania is one of the clearest examples of why published capacity does not always translate into available space. The market has tightened significantly after an estimated weekly reduction of 3,000‒4,000 TEUs of effective capacity. That reduction is not tied to one single service withdrawal. It is being driven by blank sailings, port omissions, and schedule slippage that have reduced how much capacity shippers can actually use.

North Asia to Australia and New Zealand is especially tight. Demand remains strong, all loops are full through mid-July, and roll pools are increasing out of Ningbo and Shanghai. Extra loaders and peak loaders are being deployed, but they are filling quickly and have not created meaningful space relief.

Carriers remain aligned on July peak season surcharges for northeast Asia to Australia and New Zealand. The Shanghai Containerized Freight Index (SCFI) for Australia/New Zealand is tracking roughly 40‒60% above 2025 levels and broadly in line with elevated 2024 levels.

Southeast Asia to Australia is also tightening. Recent demand recovery has pushed bookings above available space on several sailings, leaving little buffer if volumes increase further. A reopening of Middle East and Gulf flows could add another layer of pressure if cargo feeds back into Southeast Asia hubs and increases transshipment demand into Australia.

Europe to Australia remains pressured by port omissions, North European congestion, and schedule disruption. Relay options may still offer a lower-cost alternative to direct services, but they can carry additional timing and transshipment risk.

Exports out of Oceania are facing a different constraint. Seasonal commodities such as cotton and citrus are beginning to ramp up, while equipment positioning is becoming more difficult in select locations. Twenty-foot container shortages are emerging in Brisbane, Fremantle, and Adelaide, while Melbourne and Sydney remain more stable. For July, exporters should confirm availability earlier in the booking process, particularly where seasonal cargo requires 20-foot containers.

Gateway selection is key for South America West Coast

South America West Coast is not showing the same rate volatility as several other trade lanes this July, but that does not make it a low-risk market. Rates across many lanes have remained relatively stable, but reliability risks persist due to schedule disruptions, vessel rotation changes, and congestion at key transshipment points serving the region such as Manzanillo, Mexico.

The larger concern is whether cargo moves as planned. A shipment delayed by a missed connection or transshipment failure can create inventory cost, production disruption, detention fees, or customer service risk that outweighs procurement savings. That makes gateway selection more important.

Chancay is beginning to emerge as a longer-term strategic asset if direct Asia–South America West Coast services continue expanding. Cartagena also remains an underrecognized hub, with strong connectivity, capacity, reliability, and transshipment capability.

The pricing structure is also becoming more transparent, but not necessarily lower cost. Some emergency fuel surcharges are being reduced or absorbed into traditional bunker adjustment factor structures. That may simplify tariffs and improve visibility into cost components, but it does not automatically reduce total transportation cost.

For July, shippers should avoid treating stable rates as a sign that execution risk has eased. Routing reliability, transshipment exposure, and gateway selection may matter more than small differences in freight cost on lanes where schedule disruption can create larger downstream expense.

The right planning response varies by trade lane

July ocean planning should not treat all tight markets the same. Trans-Pacific and Asia–Europe are being shaped by peak-season demand, cargo pull-forward, and rate momentum. Trans-Atlantic westbound is being held tighter by capacity removal. Oceania is constrained by schedule disruption and reduced usable space. The Indian Subcontinent is being pressured by service withdrawals, booking controls, and equipment shortages. South America West Coast remains relatively stable on rates but exposed to network reliability risk.

That means the planning response should differ by trade lane. Shippers should not only ask whether space is available. They should ask why space is tight; how long that pressure may last; whether capacity relief is likely to be temporary or sustained; and whether the lowest available rate comes with routing, reliability, or timing trade-offs.

July ocean freight is not simply entering peak season. It is moving through an uneven timing cycle where some pressure may fade quickly, some may persist through carrier controls, and some may shift again if Middle East and Suez routing conditions improve. The strongest July planning advantage will come from identifying the constraint before cargo is ready, then matching the booking, routing, and equipment plan to that specific risk.

Key takeaways

Plan by trade lane, not by one peak-season assumption

Trans-Pacific, Asia–Europe, Trans-Atlantic westbound, Indian Subcontinent, Oceania, and South America West Coast lanes are tightening for different reasons. Shippers should align each booking strategy to the specific constraint in each lane.

Identify what is driving tight capacity before booking

Some trade lanes are being shaped by peak-season volumes and cargo pull-forward, while others are being affected by blank sailings, service withdrawals, port omissions, booking controls, or container shortages. The cause determines how early shippers need to book and how much routing flexibility they need.

Book earlier where service changes have reduced options

India–U.S., India–Europe, Oceania imports, and Trans-Atlantic westbound lanes require earlier confirmation where vessel space, equipment, or sailing options are limited. Late bookings are more exposed to rollovers, extended booking windows, and routing compromises.

Watch whether early peak-season pressure lasts by lane

U.S. import pull-forward, Asia–Europe rate momentum, and European summer slowdowns could cause conditions to moderate unevenly. Shippers should avoid assuming that July’s capacity conditions will persist everywhere or ease everywhere at the same time.

Treat published capacity as directional, not guaranteed

In markets such as Oceania, blank sailings, port omissions, schedule slippage, and full extra loaders are reducing the space shippers can actually use. Booking confirmation, cargo readiness, and departure-level visibility matter more when available capacity is already absorbed.

Do not expect that an end of the Middle East conflict would create immediate relief

A reopening of the Strait of Hormuz or broader return to routings through the Suez Canal may improve the long-term outlook for shipping in the region. But safety reviews, insurance coverage, vessel redeployment, service restoration, and bunker-cost lag could delay the impact.

Balance price against routing and reliability risk

Lower rates may not create better outcomes if they come with higher transshipment exposure, weaker schedule reliability, longer booking windows, or less predictable equipment access. July planning should weigh cost against the likelihood that cargo moves as required.

Middle East reopening could ease pressure, but not immediately

Given continued hostilities in the Strait of Hormuz, access to the Persian Gulf remains closed via ocean routes for the time being. Ocean carriers continue offering alternatives for Red Sea ports using overland routes.

While awaiting a ceasefire and stable re-opening of the Strait of Hormuz, we can look ahead to what would be the next steps for ocean carriers when that time comes. A reopening of the strait and a broader return of ships through the Suez Canal would be a significant development for ocean networks, but would not mean immediate normalization of shipping in the region.

If a lasting deal were to be reached between the United States and Iran, ocean carriers are expected to proceed cautiously. Safety reviews, insurance coverage, the presence of sea mines, and the availability of vessels currently deployed elsewhere would all need to be addressed before services could be restored at scale.

If more carriers return to Suez routings, global vessel capacity could eventually expand as shorter transit times free up ship supply. However, the full effect may take months, and some impacts may not be felt until late 2026 or early 2027.

Fuel is another timing issue. Emergency bunker surcharges may phase out gradually if conditions stabilize, but adjustments are often based on prior-quarter fuel costs. That means some shippers may still face elevated fees even if spot fuel prices begin to ease, because surcharge structures may continue reflecting earlier periods of higher fuel exposure.

The practical point is that a positive geopolitical development may improve the market outlook before it improves shipment execution. Carriers may not immediately unwind surcharges, restore suspended services, or release capacity back into all affected trade lanes. Shippers should continue planning around current routing, capacity, and fuel-cost exposure until service restoration becomes visible at the sailing level.

Notable shifts this month

Global: Schedule reliability should carry more weight in routing decisions

Overall global schedule reliability improved slightly in April, but performance still varies meaningfully by carrier and alliance. Gemini Cooperation remains the strongest performer, followed by MSC and CMA CGM. For shippers, the planning implication is not simply whether the market is improving. Schedule reliability should be evaluated alongside rates, capacity, routing, and transit time, particularly on lanes where missed connections, reliance on transshipping, or narrow delivery windows can create higher downstream cost.

U.S. exports: Container shortages are becoming a booking constraint

While overall U.S. import volumes rebounded in May, container availability for exports remains uneven. Weaker import flows into certain inland rail locations are contributing to container shortages for some shippers. For July export planning, confirm container availability before booking and identify backups where containers aren’t positioned near ready cargo. Options may include street turns, alternative rail ramps, or a truck-and-transload solution.

Container access should be treated as part of the booking plan, not a problem to solve after space is secured.

U.S.–Asia: Added services do not mean broader routing flexibility

New and returning services are improving options in select lanes, including direct Japan coverage from the USWC and the return of MSC’s Pearl service into south China. However, direct service options to parts of southeast Asia are narrowing, including Singapore, Thailand, and Malaysia. Shippers should confirm whether existing routings still support required transit time, reliability, and transshipment exposure.

U.S.–South America: Service changes are affecting specific port pairs

Several service updates are changing direct coverage and routings across U.S.–South America lanes. The removal of Buenaventura from a direct service reduces options from the USEC to Colombia, while South America East Coast service changes are altering coverage for ports such as Itajaí, Navegantes, Montevideo, Rio Grande, Buenos Aires, Santos, and Port Everglades.

These updates may not affect every shipper equally, but shippers with fixed port-pair requirements should confirm whether their preferred direct option still operates as expected.

Planning ahead

Confirm equipment before finalizing export bookings

For U.S. export cargo moving through inland rail locations, shippers should verify container availability early and identify backup options before cargo release. Those options may include alternate carriers, street turns, or truck-and-transload solutions when equipment is not positioned at the preferred origin.

Recheck U.S.–Asia routings by destination, not only by trade lane

Added services may improve options into select north Asia markets, but reduced direct coverage into parts of southeast Asia could change the routing profile for specific destinations. Shippers should confirm whether current routings still meet transit time, reliability, and transshipment requirements.

Use schedule reliability as part of the routing decision

Rate and capacity remain important, but they should be evaluated alongside carrier schedule performance, alliance structure, transshipment risks, and delivery-window sensitivity. This is especially important where a missed connection or delayed arrival could create inventory, production, or customer-service consequences.

Validate port-pair coverage on U.S.–South America lanes

Service changes are affecting direct coverage into select Colombia and South America East Coast ports. Shippers relying on specific port pairs should confirm whether the direct service, port call, or transshipment plan has changed before assuming prior routings are still available.

Build routing alternatives before cargo is at risk

Where container access, direct service coverage, or schedule reliability is less predictable, shippers should identify acceptable secondary routings in advance. The practical goal is to avoid making routing decisions only after the preferred option is no longer workable.

Align booking strategy with shipment sensitivity

Cargo tied to production schedules, fixed delivery windows, or customer commitments should receive earlier space, equipment, and routing confirmation than freight with more flexible timing. Not every shipment needs the same level of protection, but the difference should be intentional

Actionable freight insights

Actionable freight insights